![]()

|

|

| Re: Medicare Advantage now under threat of attack by ACA (1106303) | |

|

|

|

| Home > OTChat | |

[ Post a New Response | Return to the Index ]

|

Page 17 of 25 |

||

| (1158145) | |

Re: Medicare Advantage now under threat of attack by ACA |

|

|

Posted by Olog-hai on Sat Feb 22 14:49:19 2014, in response to Re: Medicare Advantage now under threat of attack by ACA, posted by Train Dude on Sat Feb 22 14:48:47 2014. . . . even though not a single Republican has a hand in it. |

|

| (1158147) | |

Re: Medicare Advantage now under threat of attack by ACA |

|

|

Posted by Train Dude on Sat Feb 22 14:50:53 2014, in response to Re: Medicare Advantage now under threat of attack by ACA, posted by SelkirkTMO on Sat Feb 22 14:10:03 2014. All together now, "its the Republican's fault!" |

|

| (1158181) | |

Re: Medicare Advantage now under threat of attack by ACA |

|

|

Posted by SelkirkTMO on Sat Feb 22 18:10:49 2014, in response to Re: Medicare Advantage now under threat of attack by ACA, posted by Olog-hai on Sat Feb 22 14:18:24 2014. How is Obama doing anything to Medicare going to do anything to Obamacare? Once you hit 65, no more Obamacare for you. And yes, I know that republicans voted to keep more people from MAKING IT to medicare age in the first place.Republicans run the house ... the house controls the purse strings ... the republicans can fix this. But they won't. :( |

|

| (1158191) | |

Re: Medicare Advantage now under threat of attack by ACA |

|

|

Posted by orange blossom special on Sat Feb 22 18:45:44 2014, in response to Medicare Advantage now under threat of attack by ACA, posted by Olog-hai on Sat Feb 22 11:12:14 2014. For six years he's been saying this, maybe he'll finally do the executive order.Whose first to bail bing-bong and itallianstallion out when they find out medicare bankrupts people? |

|

| (1158197) | |

Re: Medicare Advantage now under threat of attack by ACA |

|

|

Posted by bingbong on Sat Feb 22 18:53:05 2014, in response to Re: Medicare Advantage now under threat of attack by ACA, posted by orange blossom special on Sat Feb 22 18:45:44 2014. Prove that last statement. Post 2010, preferably. |

|

| (1159924) | |

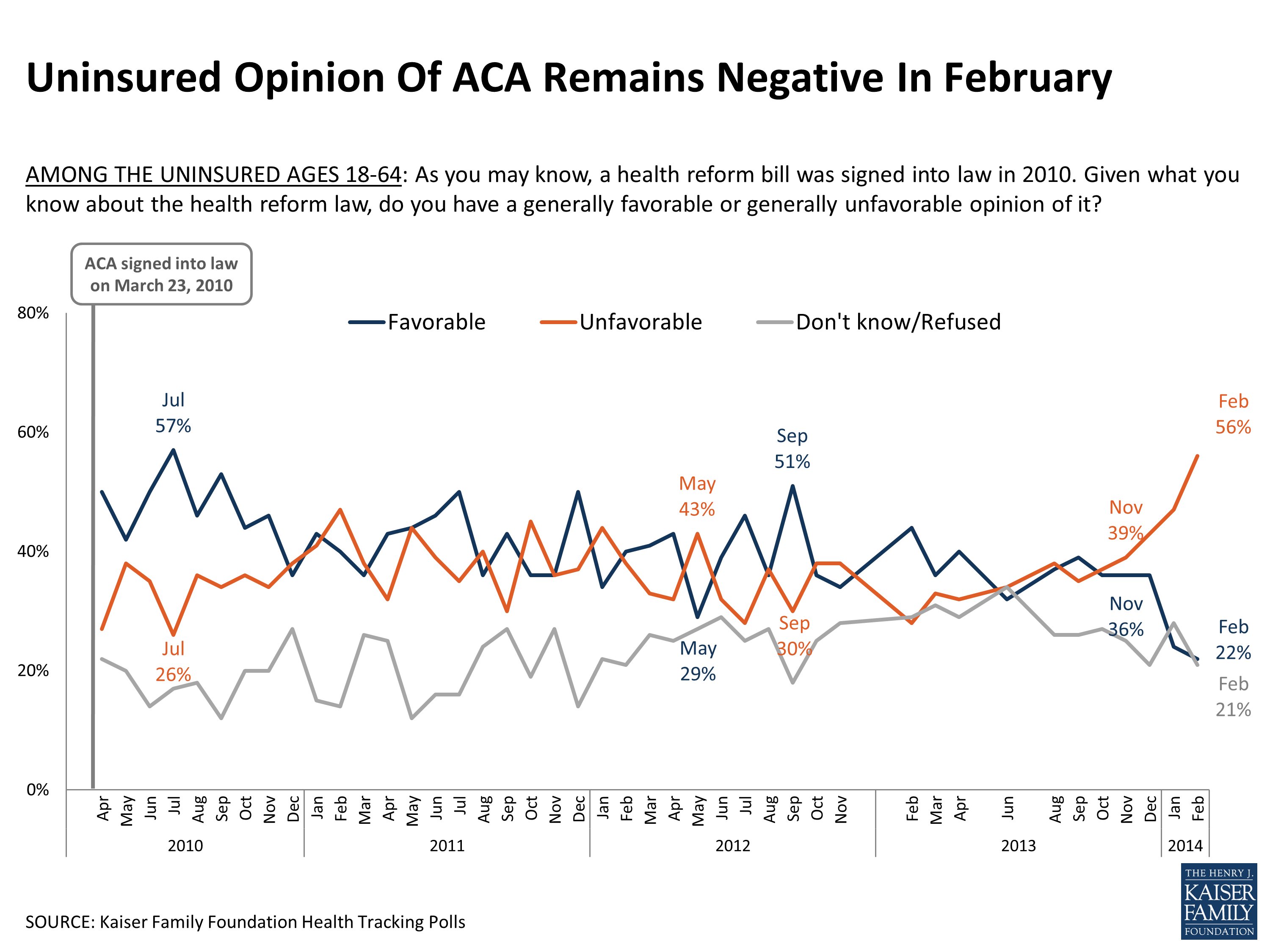

Uninsured turning against ACA; "increasingly suspicious" |

|

|

Posted by Olog-hai on Thu Feb 27 15:22:31 2014, in response to Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by SMAZ on Tue Oct 1 13:19:06 2013. Huffington Post

|

|

| (1160465) | |

Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Olog-hai on Sat Mar 1 16:07:23 2014, in response to Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by SMAZ on Tue Oct 1 13:19:06 2013. |

|

| (1160468) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Chris R16/R2730 on Sat Mar 1 16:26:53 2014, in response to Biden tries to sign up girl from *Canada* for ACA, posted by Olog-hai on Sat Mar 1 16:07:23 2014. Yet the woman who accurately predicted current events 6 years ago is a total moron and would have made a horrible VP.>inb4 butthurt |

|

| (1160494) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by AlM on Sat Mar 1 17:40:35 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Chris R16/R2730 on Sat Mar 1 16:26:53 2014. Thank you for explaining so succinctly what President McCain would have done differently that would have prevented the Russian incursion into Crimea. |

|

| (1160500) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Easy on Sat Mar 1 18:02:38 2014, in response to Biden tries to sign up girl from *Canada* for ACA, posted by Olog-hai on Sat Mar 1 16:07:23 2014. Haha! She didn't want to embarrass him!I still like Obamacare though. Even with it's many flaws it's a step in the right direction. |

|

| (1160508) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by SelkirkTMO on Sat Mar 1 18:26:45 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Chris R16/R2730 on Sat Mar 1 16:26:53 2014. Congratulations, Sarah Palin, on your broken clock award! :)

|

|

| (1160521) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by ChicagoMotorman on Sat Mar 1 19:09:15 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Chris R16/R2730 on Sat Mar 1 16:26:53 2014. Chris, you just jumped the shark. |

|

| (1160523) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by AEM-7AC #901 on Sat Mar 1 19:20:08 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Chris R16/R2730 on Sat Mar 1 16:26:53 2014. Yet the woman who accurately predicted current events 6 years ago is a total moronExcept given that we're dealing with the Russians, what were our solutions? Some weak sanctions on them? Some moral posturing? Handing over some weapons to the Georgians who'd still end up losing? At this point, screw the Georgians. They're not "white", and I'm not going to start a war over them, and the same is true for the Ukrainians. Hard realism is how you run foreign policy, not drunken flights of interventionist fantasy or naive isolationist policy. |

|

| (1160527) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Spider-Pig on Sat Mar 1 19:32:09 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by AEM-7AC #901 on Sat Mar 1 19:20:08 2014. They're not "white"But they're Caucasian. Thank you for admitting that term is BS. |

|

| (1160528) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Spider-Pig on Sat Mar 1 19:33:47 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by ChicagoMotorman on Sat Mar 1 19:09:15 2014. Why? He was being ironic. |

|

| (1160529) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Easy on Sat Mar 1 19:37:33 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Spider-Pig on Sat Mar 1 19:32:09 2014. They aren't white? Says who? |

|

| (1160530) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Spider-Pig on Sat Mar 1 19:38:03 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Easy on Sat Mar 1 19:37:33 2014. AEM-7AC #901 |

|

| (1160531) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Easy on Sat Mar 1 19:40:07 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Spider-Pig on Sat Mar 1 19:38:03 2014. They're Caucasian, but are they aryan? |

|

| (1160532) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Spider-Pig on Sat Mar 1 19:41:27 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Easy on Sat Mar 1 19:40:07 2014. No, that's iRan. |

|

| (1160533) | |

Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov |

|

|

Posted by Jeff Rosen on Sat Mar 1 19:56:27 2014, in response to Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by SMAZ on Tue Oct 1 13:19:06 2013. Honest mistake. |

|

| (1160536) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Jeff Rosen on Sat Mar 1 20:13:02 2014, in response to Biden tries to sign up girl from *Canada* for ACA, posted by Olog-hai on Sat Mar 1 16:07:23 2014. Honest mistake. |

|

| (1160537) | |

Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov |

|

|

Posted by Jeff Rosen on Sat Mar 1 20:15:36 2014, in response to Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by Jeff Rosen on Sat Mar 1 19:56:27 2014. Meant to respond to "Biden tries to sign up girl from *Canada* for ACA". That's what happens when someone changes the name of a thread and I hit "First in Thread" to respond. |

|

| (1160542) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by DAnD124 on Sat Mar 1 20:34:20 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Chris R16/R2730 on Sat Mar 1 16:26:53 2014. yes, had Palin been VP Putin would have been so afraid of her watching him from her house in Alaska that he wouldn't have tried anything |

|

| (1160549) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Olog-hai on Sat Mar 1 21:19:56 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Chris R16/R2730 on Sat Mar 1 16:26:53 2014. Yeah; you can't get a lib to change its views, even when "mugged by reality". |

|

| (1160551) | |

Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov |

|

|

Posted by Olog-hai on Sat Mar 1 21:21:36 2014, in response to Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by Jeff Rosen on Sat Mar 1 20:15:36 2014. Why would you hit "First in thread" to respond at all? |

|

| (1160553) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Olog-hai on Sat Mar 1 21:22:05 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Jeff Rosen on Sat Mar 1 20:13:02 2014. Yeah, sure. |

|

| (1160576) | |

Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov |

|

|

Posted by Jeff Rosen on Sat Mar 1 22:14:14 2014, in response to Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by Olog-hai on Sat Mar 1 21:21:36 2014. Absent mindedness I guess. I be getting old!!! |

|

| (1160587) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by Edwards! on Sun Mar 2 01:37:59 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Chris R16/R2730 on Sat Mar 1 16:26:53 2014. LOL..Canada has a health care system just as good as ours,if not better. Is That the reason why so many Americans crossed the border Before the healthcare act passed? |

|

| (1160589) | |

Re: Biden tries to sign up girl from *Canada* for ACA |

|

|

Posted by SelkirkTMO on Sun Mar 2 01:48:53 2014, in response to Re: Biden tries to sign up girl from *Canada* for ACA, posted by Edwards! on Sun Mar 2 01:37:59 2014. Shhhh! Nobody's supposed to know about that - word on the street is that it's the opposite. :) |

|

| (1160608) | |

Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov |

|

|

Posted by Dave on Sun Mar 2 07:39:39 2014, in response to Re: Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by Jeff Rosen on Sat Mar 1 22:14:14 2014. Sarge, you're as young as the woman you feel! |

|

| (1160754) | |

15,000 applicants "stuck" in Washington state health insurance exchange |

|

|

Posted by Olog-hai on Sun Mar 2 22:50:20 2014, in response to Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by SMAZ on Tue Oct 1 13:19:06 2013. Seattle Times

|

|

| (1160908) | |

Re: 15,000 applicants ''stuck'' in Washington state health insurance exchange |

|

|

Posted by Dan Lawrence on Mon Mar 3 12:06:17 2014, in response to 15,000 applicants "stuck" in Washington state health insurance exchange, posted by Olog-hai on Sun Mar 2 22:50:20 2014. They ain't the only one!! Maryland can't and probably most of the other states might be in the same problem. |

|

| (1162379) | |

"Big punt" (delay of individual mandate) looming? |

|

|

Posted by Olog-hai on Thu Mar 6 21:23:51 2014, in response to Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by SMAZ on Tue Oct 1 13:19:06 2013. Washington (goal)Post

|

|

| (1162386) | |

Re: ''Big punt'' (delay of individual mandate) looming? |

|

|

Posted by SelkirkTMO on Thu Mar 6 21:35:34 2014, in response to "Big punt" (delay of individual mandate) looming?, posted by Olog-hai on Thu Mar 6 21:23:51 2014. Heh. And you keep insisting that WaPo is "liberal." Unless YOU wrote the last couple of grafs, I think we can put THAT baby to bed now. |

|

| (1162422) | |

Re: ''Big punt'' (delay of individual mandate) looming? |

|

|

Posted by italianstallion on Fri Mar 7 00:02:33 2014, in response to "Big punt" (delay of individual mandate) looming?, posted by Olog-hai on Thu Mar 6 21:23:51 2014. Not gonna happen. |

|

| (1162508) | |

Is the POTUS losing faith in the ACA? |

|

|

Posted by Olog-hai on Fri Mar 7 13:28:04 2014, in response to Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by SMAZ on Tue Oct 1 13:19:06 2013. Yahoo Finance | The Exchange

|

|

| (1162510) | |

Re: Is the POTUS losing faith in the ACA? |

|

|

Posted by ChicagoMotorman on Fri Mar 7 13:38:40 2014, in response to Is the POTUS losing faith in the ACA?, posted by Olog-hai on Fri Mar 7 13:28:04 2014. Why are you posting this when post people here (not me) will disagree with this? |

|

| (1162538) | |

Re: Is the POTUS losing faith in the ACA? |

|

|

Posted by Olog-hai on Fri Mar 7 15:17:45 2014, in response to Re: Is the POTUS losing faith in the ACA?, posted by ChicagoMotorman on Fri Mar 7 13:38:40 2014. You just answered your own question. |

|

| (1162628) | |

Re: Is the POTUS losing faith in the ACA? |

|

|

Posted by italianstallion on Fri Mar 7 19:36:24 2014, in response to Is the POTUS losing faith in the ACA?, posted by Olog-hai on Fri Mar 7 13:28:04 2014. Uh, no. |

|

| (1162855) | |

ACA squeezing middle class in California |

|

|

Posted by Olog-hai on Sat Mar 8 13:53:11 2014, in response to Universal Health Care is HERE in these USA! Apply Now. www.healthcare.gov, posted by SMAZ on Tue Oct 1 13:19:06 2013. Guess it ain't "universal" health care after all.Sacramento Bee

|

|

| (1162858) | |

Re: ACA squeezing middle class in California |

|

|

Posted by SelkirkTMO on Sat Mar 8 14:00:58 2014, in response to ACA squeezing middle class in California, posted by Olog-hai on Sat Mar 8 13:53:11 2014. Someone should tell them that these are conservative times. They should work harder. :) |

|

| (1162863) | |

Re: ACA squeezing middle class in California |

|

|

Posted by Fred G on Sat Mar 8 14:04:04 2014, in response to Re: ACA squeezing middle class in California, posted by SelkirkTMO on Sat Mar 8 14:00:58 2014. People should just stop doing what makes them poor :)your pal, Fred |

|

| (1162865) | |

Re: ACA squeezing middle class in California |

|

|

Posted by Olog-hai on Sat Mar 8 14:10:16 2014, in response to Re: ACA squeezing middle class in California, posted by SelkirkTMO on Sat Mar 8 14:00:58 2014. No, it's more like communism. Remember?

|

|

| (1162866) | |

Re: ACA squeezing middle class in California |

|

|

Posted by Easy on Sat Mar 8 14:10:35 2014, in response to Re: ACA squeezing middle class in California, posted by Fred G on Sat Mar 8 14:04:04 2014. Cut back on some of that food and housing. Then they could pay more in sales tax so that the wealthy could pay less tax. |

|

| (1162867) | |

Re: ACA squeezing middle class in California |

|

|

Posted by SelkirkTMO on Sat Mar 8 14:10:43 2014, in response to Re: ACA squeezing middle class in California, posted by Fred G on Sat Mar 8 14:04:04 2014. Exactly! And don't get sick, and don't retire. :) |

|

| (1162869) | |

Re: ACA squeezing middle class in California |

|

|

Posted by SelkirkTMO on Sat Mar 8 14:13:17 2014, in response to Re: ACA squeezing middle class in California, posted by Olog-hai on Sat Mar 8 14:10:16 2014. I always knew today's conservatives were communists. We can see it at work now in Ukraine. |

|

| (1162870) | |

Re: ACA squeezing middle class in California |

|

|

Posted by SelkirkTMO on Sat Mar 8 14:14:03 2014, in response to Re: ACA squeezing middle class in California, posted by Easy on Sat Mar 8 14:10:35 2014. THIW. Gotta make sacrifices so Karl Icahn can raise his dividend. |

|

| (1162872) | |

Re: ACA squeezing middle class in California |

|

|

Posted by Fred G on Sat Mar 8 14:18:08 2014, in response to Re: ACA squeezing middle class in California, posted by Easy on Sat Mar 8 14:10:35 2014. If they would just buy RV's and consolidate housing and transportation, then they could probably afford to eat better and buy more stuff.your pal, Fred |

|

| (1162873) | |

Re: ACA squeezing middle class in California |

|

|

Posted by salaamallah@hotmail.com on Sat Mar 8 14:20:15 2014, in response to Re: ACA squeezing middle class in California, posted by SelkirkTMO on Sat Mar 8 14:10:43 2014. big iawtp |

|

| (1162932) | |

Re: ACA squeezing middle class in California |

|

|

Posted by SelkirkTMO on Sat Mar 8 18:57:01 2014, in response to Re: ACA squeezing middle class in California, posted by Fred G on Sat Mar 8 14:18:08 2014. Plus live in WalMart parking lots so they can save on gas. :) |

|

|

Page 17 of 25 |

||